Fixed Income: Bullet versus Barbell Bond Portfolio (FRM T4-40)

Vložit

- čas přidán 31. 05. 2024

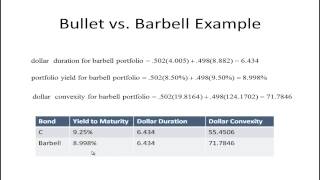

- The bullet portfolio invests in a single medium-term bond. The corresponding barbell portfolio invests the same amount of capital and achieves the same duration, but invests in a mix of the short-term plus long-term bond. But the barbell portfolio will have greater convexity. Tuckman explains: "The barbell has greater convexity than the bullet because duration increases linearly with maturity while convexity increases with the square of maturity. If a combination of short and long durations, essentially maturities, equals the duration of the bullet, that same combination of the two convexities, essentially maturities squared, must be greater than the convexity of the bullet."

💡 Discuss this video here in our FRM forum: trtl.bz/2XIHmn3.

📗 You can find Tuckman's Fixed Income Securities book here: amzn.to/2SOMGzv

👉 Subscribe here / bionicturtl. .

to be notified of future tutorials on expert finance and data science, including the Financial Risk Manager (FRM), the Chartered Financial Analyst (CFA), and R Programming!

❓ If you have questions or want to discuss this video further, please visit our support forum (which has over 50,000 members) located at bionicturtle.com/forum

🐢 You can also register as a member of our site (for free!) at www.bionicturtle.com/register/

📧 Our email contact is support@bionicturtle.com (I can also be personally reached at davidh@bionicturtle.com)

For other videos in our Financial Risk Manager (FRM) series, visit these playlists:

Texas Instruments BA II+ Calculator

• Texas Instruments BA I...

Risk Foundations (FRM Topic 1)

• Risk Foundations (FRM ...

Quantitative Analysis (FRM Topic 2)

• Quantitative Analysis ...

Financial Markets and Products: Intro to Derivatives (FRM Topic 3, Hull Ch 1-7)

• Financial Markets and ...

Financial Markets and Products: Option Trading Strategies (FRM Topic 3, Hull Ch 10-12)

• Financial Markets and ...

FM&P: Intro to Derivatives: Exotic options (FRM Topic 3)

• FM&P: Intro to Derivat...

Valuation and Risk Models (FRM Topic 4)

• Valuation and RIsk Mod...

Coming Soon ....

Market Risk (FRM Topic 5)

Credit Risk (FRM Topic 6)

Operational Risk (FRM Topic 7)

Investment Risk (FRM Topic 8)

Current Issues (FRM Topic 9)

For videos in our Chartered Financial Analyst (CFA) series, visit these playlists:

Chartered Financial Analyst (CFA) Level 1 Volume 1

• Level 1 Chartered Fina...

#bionicturtle #risk #financialriskmanager #FRM #finance #expertfinance

Our videos carefully comply with U.S. copyright law which we take seriously. Any third-party images used in this video honor their specific license agreements. We occasionally purchase images with our account under a royalty-free license at 123rf.com (see www.123rf.com/license.php); we also use free and purchased images from our account at canva.com (see about.canva.com/license-agree.... In particular, the new thumbnails are generated in canva.com. Please contact support@bionicturtle.com or davidh@bionicturtle.com if you have any questions, issues or concerns.

In the video, I said I would explain how I solved for the amount that should be invested in the short-term bond in order to achieve a duration with the barbell portfolio that matches the duration of the bullet portfolio. The key is to match dollar durations because if the dollar durations match, then the durations match (given the investment dollars are the same). Dollar duration equals investment multiplied by modified duration; that is, let D = modified duration and let V = value of dollars invested, such that DV = dollar duration. Further, define S = duration of short-term bond; M = duration of (bullet) medium-term bond; and L = duration of long-term bond. The dollar duration, then, of the bullet portfolio is simply V*M or, in my example, 63.763*15 = 956.44 million. The dollar duration of the barbell portfolio is given by S*V(small) + L*V(large), where V(small) and V(large) are the respective dollar investments. However, we require that V(small) + V(large) = V, and V(large) = V - V(small) such that the dollar duration of the barbell is given by S*V(small) + L*[V - V(small)]. Then the equality is given by: S*V(small) + L*[V - V(small)] = M*V --> S*V(small) + L*V - L*V(small)] = M*V --> V(small)*(S-L) + L*V = M*V --> V(small)*(S-L) = M*V - L*V --> V(small) = (M*V - L*V)/(S-L). In my example, S = 5.0, M = 15.0 and L = 30.0 such that V(small) = (15.0*V - 30*V)/(5.0 - 30.0) is the solution for V(small) as a function of V. In this case, V(small) = (15.0*63.763 - 30*63.763)/(5.0 - 30.0) = 38.26 million to the 5-year bond and the remaining 25.51 to the 30-year bond which turns out to be 60/40%. Thanks!

I have a question. In the example Tuckman table 4.7 the medium bond with 9.5 years to maturity. The yield is greater than a coupon for that bond, should we expect that the price should be below 100 (below face value)"? I understand that it might happen, but in theory it should be less than 100? Or there is some other condition in this exercise that could explain such situation?

I thought a barbell portfolio was adding more weights on the short end and long end?

Thanks again for this useful video.

Can you please help me understand that, by price of Barbel portfolio would be lower, we mean although cost of portfolio would be 63, the portfolio would be marked at Lower price?

Thanks in advance

Hi Sunil, I just showed how the YIELD of the barbell will be LESS THAN the yield of the duration-matched bullet (both invest the same capital, so their initial values are the same). This is why no free lunch: the barbell's higher convexity (compared to the bullet) implies greater gain/smaller loss under big yield changes, but it has a lower YIELD at the INITIAL rate. The idea is that, if rates are constant (or move only a little) the bullet will outperform, consistent with its higher yield; but if rates are volatile, then the barbell will outperform. Thanks,

@@bionicturtle Got it.. Thank you Sir

@@bionicturtle For bonds with different maturities if bond yields in the portfolio are not equal to each other we cannot just take weighted average of their yields to receive the portfolio yield. It can be easily checked for barbell portfolio in the example. It is necessary for portfolio yield y= 3.63% to fulfill the equation 38.26*exp(2%*5)exp(-y*5)+25.51*exp(4%*30)*exp(-y*30)=63.763 And in this particular case there is a free lunch.

@@vvvolkov Yes, excellent point! As I was following Tuckman's approach, I was using the WEIGHTED (average) yield, which is not the portfolio's yield. I agree with your calculation of the portfolio's yield to maturity (aka, IRR).