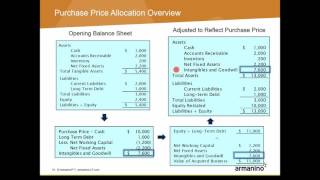

Purchase Price Allocation: Goodwill

Vložit

- čas přidán 14. 06. 2018

- In acquisition accounting, purchase price allocation is a practice in which an acquirer allocates the purchase price into the assets and liabilities of the target company acquired in the transaction.

Click here to learn more about this topic: corporatefinanceinstitute.com...

![How to Calculate Goodwill in M&A Deals and Merger Models [Tutorial]](http://i.ytimg.com/vi/m5p0D3kV72g/mqdefault.jpg)

![How to Calculate Goodwill in M&A Deals and Merger Models [Tutorial]](/img/tr.png)

Thanks for the video. Wouldn't you have to offset the goodwill by the DTL created from the step-up?

Thank you Sir

why You subtract write off Existing Goodwill? it must be added I think?

It was the Goodwill of the previous owner, it does not hold any value to the new company. A new Goodwill must be calculated based on what was bought and what was paid. The old goodwill does not meet the requirements of being classified as an intangible according to IAS 36.

@@teme2k11 Thanks

@@teme2k11 what if the old owner keeps some % of equity? Let’s say 20%. Do you have to add the old depreciation in this case?