Cointegration (Video 7 of 7 in the gretl Instructional Video Series)

Vložit

- čas přidán 16. 02. 2015

- The gretl Instructional Video Series consists of seven videos that instruct and demonstrate how to use gretl to apply econometric techniques. The videos are designed to be 'hands on' and will be the most effective if the students follow and actively participate using gretl on their own computer while watching the video. The videos can be used for individual study or for in-class presentation.

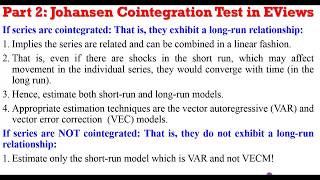

The learning objectives for Video 7 include the following: Engle-Granger Cointegration Test and Vector Error Correction (VECM) estimation.

Citation: Mann, J. (2011, September 1). Cointegration - Video 7 of 7 in the gretl Instructional Video Series. Retrieved from • Cointegration (Video 7...

It is important note that the videos are not designed to teach econometric theory and techniques, rather they apply the econometric theory and techniques learned in class.

I LOVE GRETL !!!! THIS IS KEY!

Awesome, thank you very much! It was super useful.

God bless ya janelle, thank you

thank you for this

Hi and very thanks for this video. However, as I'm a newbie (in both Gretl and Engle-Granger test), I'd like to ask the following:

1) Minute 7:45= when doing the Engle test, you include the constant but not the trend. Is there any reason?(considering previously You included both of them).

2) I'm used to follow your very same steps. but please tell me if the two alternatives I'm about to describe are the same:

Alternative A= Select both WTI and Brent and use the Gretl function "Engle-Granger Test" (as You did in the video).

Alternative B= I make an OLS regression with WTI and Brent. Then I save the residuals(errors) from the OLS regression and finally make an ADF test on residuals saved. Am I wrong in doing this two alternatives as the same thing?

3) Minute 11:48= you say to remove the constant. I honestly still don't understand....

Thanks for your time (and sorry for my english)

Hi, I'm getting an 'xmlParseFile failed' error while trying to upload a data file of my own. Could you help out on what I'm doing wrong?

Hi,

My variables show a similar order of integration I(1) using original dataset. However, running tests for individual price variables after adding logs, they show different orders of integration e.g I(0) and I(1). Is there any way to go about it? I was hoping to use a VECM to analyse the long-run relationship between my variables. Thank you

How do you tell that D is equal to 1 for both of the ADF results?

And why not a video about the GMM model?

Where is the file CrudePrice ? Including in sample Gretl files?

Thank you for the very informative video on Cointegration and ECM. Please, I need a more intuitive explanation of the Error Correction Model. Thanks once again.

Hello Mohammed Bara Adamu - The intuition being the ECM can be tricky. I suggest reading the relevant portion of the text by Verbeek (A Modern Guide to Econometrics), or Enders (Applied Econometric Time Series).

So if you have more than 5 variables, what do we do if for the cointegration test the p value is bigger than 0.05? Can we still continue and do a ECM??

Hi Bennet - Please be sure to learn econometric theory before analyzing data. The book by Enders is very good. Here, the Johansen test should be performed given you have five variables.

Good !! Sorry, Do you know how to do the procedure with the default command: VECM? please!!

Hello JJESUS - I suggest checking the gretl User's Guide (gretl.sourceforge.net/gretl-help/gretl-guide.pdf). It is very helpful!

@@JanelleMann please how do you use time dummies in gretl