How to audit financial statements | FloQast

Vložit

- čas přidán 7. 08. 2024

- 0:00 Introduction

0:20 What are Audited Financial Statements?

1:44 Top Financial statements to audit

2:25 How do auditors verify financial statements

6:17 Recap

Learn more about how to audit financial statements here: floqast.com/blog/what-is-fina...

What Are Audited Financial Statements?

An audited financial statement is any financial statement that has been officially inspected by, tested, and opined on by a certified public accountant (CPA) that is independent of the organization.

The purpose of a financial statement audit is to get an objective opinion on the organization’s financial position. Auditors don’t guarantee that every number on the financial statements is 100% accurate. Instead, they perform tests and analytical procedures that allow them to provide reasonable assurance that the financial statements are free of material misstatements and prepared following generally accepted accounting principles (GAAP).

Auditors work within an acceptable margin of error, known as materiality. Materiality depends on the size of the organization and its revenues and expenses. For a very small company, an error of a few hundred dollars might be significant. But for a company the size of Amazon or Facebook, a material misstatement might be hundreds of thousands of dollars.

Top Financial Statements to Audit

According to the Securities and Exchange Commission (SEC), most audits focus on four standard financial statements:

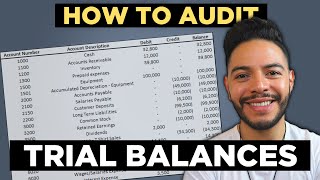

Balance Sheet. The balance sheet shows what a company owns and what it owes as of a certain date.

Income Statement. The income statement shows how much the company made and spent over a period of time.

Statement of Cash Flows. The statement of cash flows shows how cash flowed into and out of the company over a period of time.

Statement of Shareholder’s Equity. The statement of shareholder’s equity shows changes in the interests of the company’s shareholders or owners over a period of time.

How Do Auditors Verify Financial Statements?

A financial statement audit begins when an organization signs an engagement letter from its audit firm. The audit engagement letter is the contract spelling out what each party agrees to.

Audit Engagement Letter: Contract between audit firm and client

From there, the audit follows generally accepted auditing standards (GAAS), which is a four-step process.

Step 1: Assessing risk

Auditing rules require the auditor to assess general business risks and industry- and company-specific risks. The assessment helps auditors determine where to focus their audit procedures and develop appropriate procedures to minimize the potential risk of material misstatement.

The auditors may use various analytical procedures to test the company’s internal controls and identify risky areas or obvious anomalies in the numbers.

Step 2: Planning

Based on the risk assessment, the audit firm develops a detailed audit plan to test the internal control environment and investigate the accuracy of specific line items within the financial statements. The audit partner then assigns audit team members to work on each element of the plan and works with the client to develop a timeline for getting the work done.

Step 3: Gathering evidence

Fieldwork may last anywhere from one day to several months, depending on the complexity of the organization.

During fieldwork, the auditors test and analyze internal controls. The exact procedures will vary depending on the type of account being audited and the organization’s risk assessment, but usually include a mix of analytical and substantive procedures.

Step 4: Communicating the findings

At the end of the audit, the audit firm develops an “opinion” about the accuracy and integrity of the company’s financial statements. The firm then issues a report on whether the financial statements:

Four types of audit reports are possible:

Unqualified opinion. This is also called a “clean report” and means the auditors are satisfied with the company’s accounting and operations and didn’t find any material problems.

Qualified opinion. This report indicates that the auditors found problems in some type of transaction or area and aren’t confident that the accounting is correct for that specific area. The report will identify the problematic area and issues.

Disclaimer of opinion. In this situation, the auditors couldn’t obtain enough evidence to determine whether the financial statements were presented fairly or not. This may happen if management doesn’t provide the requested information or because management’s explanation didn’t make sense.

Adverse opinion. An adverse audit opinion means the auditors saw evidence of material misstatement or fraud or possibly both.

Thanks for your help

One word, Simplified