Fraud Triangle | Auditing and Attestation | CPA Exam

Vložit

- čas přidán 7. 06. 2024

- IN this video, I discuss the fraud triangle

✔️Accounting students and CPA Exam candidates, check my website for additional resources: farhatlectures.com/

📧Connect with me on social media: linktr.ee/farhatlectures

#cpaexam #accountingstudent #auditcourse

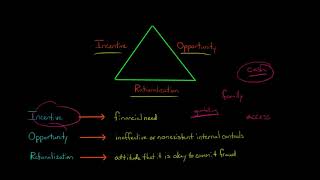

hree conditions for fraud arising from fraudulent financial reporting and misappropriations of assets are described in the auditing standards. As shown in Figure 10-1, these three conditions are referred to as the fraud triangle.

Incentives/Pressures. Management or other employees have incentives or pressures to commit fraud.

Opportunities. Circumstances provide opportunities for management or employees to commit fraud.

Attitudes/Rationalization. An attitude, character, or set of ethical values exists that allows management or employees to commit a dishonest act, or they are in an environment that imposes sufficient pressure that causes them to rationalize committing a dishonest act.

Risk Factors for Fraudulent Financial Reporting

An essential consideration by the auditor in uncovering fraud is identifying factors that increase the risk of fraud. Table 10-1 provides examples of these fraud risk factors for each of the three conditions of fraud for fraudulent financial reporting. In the fraud triangle, fraudulent financial reporting and misappropriation of assets share the same three conditions, but the risk factors differ. We’ll first address the risk factors for fraudulent financial reporting, and then discuss those for misappropriation of assets. Later in the chapter, the auditor’s use of the risk factors in uncovering fraud is discussed.

A common incentive for companies to manipulate financial statements is a decline in the company’s financial prospects. For example, a decline in earnings may threaten the company’s ability to obtain financing. Companies may also manipulate earnings to meet analysts’ forecasts or benchmarks such as prior-year earnings, to meet debt covenant restrictions, to achieve a bonus target based on earnings, or to artificially inflate stock prices. In some cases, management may manipulate earnings just to preserve their reputation. Figure 10-2 highlights KPMG’s survey finding that personal financial incentives, especially a desire to fund an extravagant lifestyle, and the need to meet pre-specified business performance targets are often cited as primary incentives to engage in fraudulent actions.

Although the financial statements of all companies are potentially subject to manipulation, the risk is greater for companies in industries where significant judgments and estimates are involved. For example, valuation of inventories is subject to greater risk of misstatement for companies with diverse inventories in many locations. The risk of misstatement of inventories is further increased if those inventories are at risk for obsolescence.

The attitude of top management toward financial reporting is a critical risk factor in assessing the likelihood of fraudulent financial statements, as illustrated by Figure 10-2. If the CEO or other top managers display a significant disregard for the financial reporting process, such as consistently issuing overly optimistic forecasts, or they are overly concerned about meeting analysts’ earnings forecasts, fraudulent financial reporting is more likely. Management’s character or set of ethical values also may make it easier for them to rationalize a fraudulent act. A sense of superiority by executives is the most commonly cited condition related to attitude and rationalization

You are awesome. Thanks

You are most welcome. Please subscribe and share. If you want to access more resources, check my website:

✔farhatlectures.com/

✔Instagram: @farhatlectures

✔ Linkedin: www.linkedin.com/in/professorfarhat/

✔Facebook:@accountinglectures

✔Twitter: @farhatlectures

🎤Email: Mansour.farhat@gmail.com

thank you sir, it helps a lot 🙏

Most welcome! Glad it was helpful! Most welcome! Please take a look at my auditing course: farhatlectures.pathwright.com/library/auditing-and-attestation-awtel/about/

Thanks!!

You are most welcome. Please subscribe and share. If you want to access more resources, check my website:

✔farhatlectures.com/

✔Instagram: @farhatlectures

✔ Linkedin: www.linkedin.com/in/professorfarhat/

✔Facebook:@accountinglectures

✔Twitter: @farhatlectures

🎤Email: Mansour.farhat@gmail.com

great

You are most welcome. Please subscribe and share.

If you want to access more resources, check my website: farhatlectures.com/

Connect with me:

Instagram Account: instagram.com/farhatlectures/

Linkedin: www.linkedin.com/in/professorfarhat/ Facebook: facebook.com/accountinglectures

Twitter: twitter.com/farhatlectures

Thank you Prof.

You are very welcome. Please visit my website for more: www.farhatlectures.com

is it just me or a sense of entitlement could be in the rationalization category as well?

Thank you sir

So nice of you! Thank you and please visit the website for more farhatlectures.com/

Ok

YOu are welcome.

Check my website for more:

✔farhatlectures.com/

✔Instagram: @farhatlectures

✔ Linkedin: www.linkedin.com/in/professorfarhat/

✔Facebook:@accountinglectures

✔Twitter: @farhatlectures

🎤Email: Mansour.farhat@gmail.com