Session 5: Equity Risk Premiums

Vložit

- čas přidán 12. 02. 2023

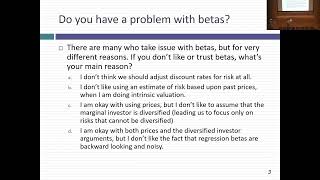

- (I apologize for the screen sharing snafu, which is about 12 minutes, between minutes 10 and 22 of the class, since you watch an awfully low res video of me in front of the classroom). In the session today, we started by doing a brief test on country risk premiums. We started with an assessment of historical equity risk premiums, and why they are not good predictors of future equity risk premiums, before embarking on a discussion of country risk and how to deal with it, and measure it. We also looked at company risk exposure to country risk, with my core argument being that a company’s exposure to country risk comes from where it dos business, not where it is incorporated:

After a brief foray into lambda, a more composite way of measuring country risk, we spent the rest of the session talking about the dynamics of implied equity risk premiums and what makes them go up, down or stay unchanged. We then moved to cross market comparisons, first by comparing the ERP to bond default spreads, then bringing in real estate risk premiums and then extending the concept to comparing ERPs across countries.

Finally, I made the argument that you should not stray too far from the current implied premium, when valuing individual companies, because doing so will make your end valuation a function of what you think about the market and the company. If you have strong views on the market being over valued or under valued, it is best to separate it from your company valuation. I am attaching the excel spreadsheet that I used to compute the implied ERP at the start of February 2023. Play with it when you get a chance. Post class test and solution attached. Until next time!

Start of the class test: www.stern.nyu.edu/~adamodar/p...

ERP for February 2023: pages.stern.nyu.edu/~adamodar...

Slides: www.stern.nyu.edu/~adamodar/p...

Post class test: www.stern.nyu.edu/~adamodar/p...

Post class test solution: www.stern.nyu.edu/~adamodar/p...

This channel is great

Cant thank you enough professor Aswath, for your kind sharing of all your valuable knowledge, you are really liberating knowledge and education for anyone who wants to learn and doesnt have the chance to join the classes physically

The legendary professor of this universe.

Love your lecture a lot. from Delhi

Hi Aswath, thanks for an informative upload, I'm always fascinated by the principles of valuation🙏

This is gold!

History will remember him as one of the great

Thank you!

The Royal Dutch Shell example makes most sense to me but is not included in the final list of approaches somehow.

Why there are few different Session 5 versions?

different courses - different sessions

Mr. Damodaran recommends to select a playlist and stick to. This video is part of "Valuation MBA Spring 2023"

How did he get the 5.95% erp?

For US right?

Can you rename Czech Republic to Czechia and Swaziland to Eswatini.