- 90

- 2 454 058

QuantPy

Australia

Registrace 23. 06. 2017

This channel is all about learning quantitative finance with python.

So many channels, books, people, and even universities out there only explain financial concepts, but don't show how to implement these concepts in a meaningful and practical way. Here I aim to implement financial concepts with Python, because I believe the best way to learn is to Build Something!

My name is Jonathon Emerick and despite studying a Bachelor of Chemical Engineering and a Master in Financial Mathematics, I felt that I hadn't learned how to address real world problems or gained the skills required for success in the financial industry.

On this channel I try to fill the gaps in my own knowledge, while helping others with concepts that I have only solidified after leaving university. This channel keeps me accountable, and I hope you can gain value or insight from these learnings. Try searching on the channel page, or via quantpy.com.au/

So many channels, books, people, and even universities out there only explain financial concepts, but don't show how to implement these concepts in a meaningful and practical way. Here I aim to implement financial concepts with Python, because I believe the best way to learn is to Build Something!

My name is Jonathon Emerick and despite studying a Bachelor of Chemical Engineering and a Master in Financial Mathematics, I felt that I hadn't learned how to address real world problems or gained the skills required for success in the financial industry.

On this channel I try to fill the gaps in my own knowledge, while helping others with concepts that I have only solidified after leaving university. This channel keeps me accountable, and I hope you can gain value or insight from these learnings. Try searching on the channel page, or via quantpy.com.au/

From Black Holes to Black-Scholes

EP 003 QuantPy Insights Podcast | Davide Bufalini | The Journey from Academia to Quant Finance

📈 About This Episode:

Today, we have a very special guest, Davide Bufalini, who has transitioned from academia having studied a PhD in theoretical physics to the world of quantitative finance. In this episode, we discuss some of the largest challenges, transferrable skills and recommendations for making the transition from university to the quant industry.

🔑 Key Takeaways (Guest Perspective):

From solving one of the biggest challenges in theoretical physics to understanding market flows and behaviour, what I learned in my PhD applies to my job on a daily basis. To successfully transition to quant finance, it is crucial to have the right motivations, strong math fundamentals, have studied the right books, and have asked experienced practitioners about their opinions at the right time.

🎯 Who Should Watch?

If you're a university student/researcher intrigued by a career in quantitative finance, or a seasoned quant looking to diversify your skill set and advance your career, this episode is for you!

🏛 Guest Background, Motivations, Insights and Resources (Guest Perspective)

My PhD focused on one of the biggest challenges in theoretical physics: solving the black hole information paradox, first formulated by Stephen Hawking. I contributed to this issue within the framework of string theory, today's leading theory of quantum gravity.

Despite the stimulating and interesting topic, the academic lifestyle was not something that I wanted to pursue because of many issues, unfortunately common to numerous researchers. While deciding to change career, I learned more about the fascinating world of quant finance, how I could continue to have fun with math, and apply my skills to new exciting challenges.

🎓 Useful skillset from PhD to Quant?

From solving supergravity equations to the Black-Scholes’ PDE, from expectations values of operator products to expectations under martingale measures, the overlap between the fields is broader than what it seems at first glance. Problem-solving skills, research abilities, statistical physics, differential equations, Fourier transforms, and Lebesgue integrals: all of these concepts apply to my job, and help in understand research papers and books with relative ease.

🔋 What skillset do you use every day?

Daily, I program in Python and use traditional and stochastic calculus to actively produce work. To read and understand research papers, knowledge of hypergeometric functions and complex analysis has been proven useful. Most importantly, my approach to solving problems is still very similar to that of the PhD, and the rigorous imprint and technical background is likewise crucial in a field such as quantitative finance.

📚 Recommended Books & Resources

BASICS & OPTION PRICING

1. Wilmott - Paul Wilmott introduces Quantitative Finance

2. Baxter, Rennie - Financial Calculus

3. Bjork - Arbitrage Theory in Continuous Time

4. The two books by Steven Shreve (a classic!)

I strongly recommend following the above order, and I recommend studying the Black-Scholes model and the Greeks, as a minimum requirement. Note that the list is non-exhaustive.

5. [Advanced, and only for physicists with a strong math background] Labordere - Analysis, Geometry, and Modeling in Finance: Advanced Methods in Option Pricing

INTERVIEWS

- Joshi, Denson, Downes - Quant Job Interview Questions And Answers

- Crack - Heard on the Street: Quantitative Questions from Wall Street Job Interviews

- Wilmott - Frequently Asked Questions in Quantitative Finance

CODING SKILLS

- Python for research and AI, machine learning, and deep learning.

- C++ or other low latency language for front office roles

- Big banks and institutions may have their proprietary programming language, so understanding the logic behind programming and algorithms is crucial.

★ ★ QuantPy GitHub ★ ★

Collection of resources used on QuantPy CZcams channel. github.com/thequantpy

★ ★ Discord Community ★ ★

Join a small niche community of like-minded quants on discord. discord.com/invite/aY2Af4CxHP

★ ★ CONTACT US ★ ★

EMAIL: pythonforquants@gmail.com

Disclaimer: All ideas, opinions, recommendations and/or forecasts, expressed or implied in this content, are for informational and educational purposes only and should not be construed as financial product advice or an inducement or instruction to invest, trade, and/or speculate in the markets. Any action or refraining from action; investments, trades, and/or speculations made in light of the ideas, opinions, and/or forecasts, expressed or implied in this content, are committed at your own risk an consequence, financial or otherwise. As an affiliate of ThetaData, QuantPy Pty Ltd is compensated for any purchases made through the link provided in this description.

📈 About This Episode:

Today, we have a very special guest, Davide Bufalini, who has transitioned from academia having studied a PhD in theoretical physics to the world of quantitative finance. In this episode, we discuss some of the largest challenges, transferrable skills and recommendations for making the transition from university to the quant industry.

🔑 Key Takeaways (Guest Perspective):

From solving one of the biggest challenges in theoretical physics to understanding market flows and behaviour, what I learned in my PhD applies to my job on a daily basis. To successfully transition to quant finance, it is crucial to have the right motivations, strong math fundamentals, have studied the right books, and have asked experienced practitioners about their opinions at the right time.

🎯 Who Should Watch?

If you're a university student/researcher intrigued by a career in quantitative finance, or a seasoned quant looking to diversify your skill set and advance your career, this episode is for you!

🏛 Guest Background, Motivations, Insights and Resources (Guest Perspective)

My PhD focused on one of the biggest challenges in theoretical physics: solving the black hole information paradox, first formulated by Stephen Hawking. I contributed to this issue within the framework of string theory, today's leading theory of quantum gravity.

Despite the stimulating and interesting topic, the academic lifestyle was not something that I wanted to pursue because of many issues, unfortunately common to numerous researchers. While deciding to change career, I learned more about the fascinating world of quant finance, how I could continue to have fun with math, and apply my skills to new exciting challenges.

🎓 Useful skillset from PhD to Quant?

From solving supergravity equations to the Black-Scholes’ PDE, from expectations values of operator products to expectations under martingale measures, the overlap between the fields is broader than what it seems at first glance. Problem-solving skills, research abilities, statistical physics, differential equations, Fourier transforms, and Lebesgue integrals: all of these concepts apply to my job, and help in understand research papers and books with relative ease.

🔋 What skillset do you use every day?

Daily, I program in Python and use traditional and stochastic calculus to actively produce work. To read and understand research papers, knowledge of hypergeometric functions and complex analysis has been proven useful. Most importantly, my approach to solving problems is still very similar to that of the PhD, and the rigorous imprint and technical background is likewise crucial in a field such as quantitative finance.

📚 Recommended Books & Resources

BASICS & OPTION PRICING

1. Wilmott - Paul Wilmott introduces Quantitative Finance

2. Baxter, Rennie - Financial Calculus

3. Bjork - Arbitrage Theory in Continuous Time

4. The two books by Steven Shreve (a classic!)

I strongly recommend following the above order, and I recommend studying the Black-Scholes model and the Greeks, as a minimum requirement. Note that the list is non-exhaustive.

5. [Advanced, and only for physicists with a strong math background] Labordere - Analysis, Geometry, and Modeling in Finance: Advanced Methods in Option Pricing

INTERVIEWS

- Joshi, Denson, Downes - Quant Job Interview Questions And Answers

- Crack - Heard on the Street: Quantitative Questions from Wall Street Job Interviews

- Wilmott - Frequently Asked Questions in Quantitative Finance

CODING SKILLS

- Python for research and AI, machine learning, and deep learning.

- C++ or other low latency language for front office roles

- Big banks and institutions may have their proprietary programming language, so understanding the logic behind programming and algorithms is crucial.

★ ★ QuantPy GitHub ★ ★

Collection of resources used on QuantPy CZcams channel. github.com/thequantpy

★ ★ Discord Community ★ ★

Join a small niche community of like-minded quants on discord. discord.com/invite/aY2Af4CxHP

★ ★ CONTACT US ★ ★

EMAIL: pythonforquants@gmail.com

Disclaimer: All ideas, opinions, recommendations and/or forecasts, expressed or implied in this content, are for informational and educational purposes only and should not be construed as financial product advice or an inducement or instruction to invest, trade, and/or speculate in the markets. Any action or refraining from action; investments, trades, and/or speculations made in light of the ideas, opinions, and/or forecasts, expressed or implied in this content, are committed at your own risk an consequence, financial or otherwise. As an affiliate of ThetaData, QuantPy Pty Ltd is compensated for any purchases made through the link provided in this description.

zhlédnutí: 10 824

Video

OpenAI & Python: The Ultimate Twitter Automation Guide

zhlédnutí 6KPřed 7 měsíci

In this tutorial, we dive into automating your Twitter feed by leveraging OpenAI's Chat GPT, Python, and the Tweepy module. The bot is designed to generate tweets from a list of quantitative Python ideas using a specialized OpenAI prompt template. All of this is set up in a Jupyter Notebook environment for easy testing and modification. Tweets are then scheduled to be posted every 12 hours usin...

A 20-Year Veteran Reveals the World of Options Market Making

zhlédnutí 36KPřed 8 měsíci

EP 002 QuantPy Insights Podcast | Anonymous Guest Welcome back to the second episode of QuantPy Insights, where we dissect the complex world of quantitative finance and break it down for you! 📈 About This Episode: Today, we have a very special guest who has spent over two decades in the fast-paced realm of options market making. We dig deep into the intricacies of market making, from how firms ...

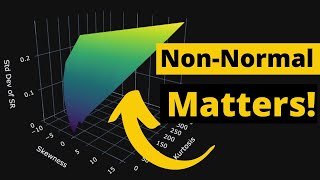

Is your Sharpe Ratio is Lying to you? Use this instead

zhlédnutí 6KPřed 8 měsíci

“Although skewness and kurtosis does not affect the point estimate of Sharpe ratio, it greatly impacts its confidence bands, and consequently its statistical significance” Bailey and López de Prado (2012). In the last video we explained the downfalls of relying on the Central Limit Theorem (CLT) and using the mean and standard deviation to calculate a point estimate of the Sharpe Ratio. In this...

You will need to be the kind of person who loves to solve problems · Octavio Baraldo Queijeiro

zhlédnutí 10KPřed 8 měsíci

EP 001 QuantPy Insights Podcast | Octavio Baraldo Queijeiro Octavio began his journey in quantitative finance after completing a mathematically-oriented economics undergraduate program in Argentina. Intrigued by the rapidly evolving landscape and machine learning developments he witnessed in China, his curiosity steered him toward the field of quantitative finance. Armed with this newfound moti...

Stop making investment decisions using this metric!

zhlédnutí 8KPřed 8 měsíci

The Pitfalls of Relying on the Central Limit Theorem in Portfolio Return Analysis. In the world of finance, both individuals and investing professionals alike strive for making sound investment decisions with consideration of risk. Usually this process involves understanding and analysis of portfolio returns. Central to this methodology is the Central Limit Theorem (CLT), a statistical concept ...

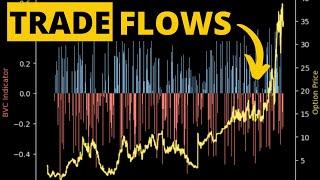

Inferring the Aggressor using Options Data

zhlédnutí 12KPřed rokem

We will be implementing the bulk volume classification algorithm to attempt to discern information from tick by tick trade data. We will be using ThetaData's API which provides both Historical and Real-time Streaming of Options Tick Level Data! We first explore what algorithms have been used previously to attempt to infer the aggressor (the trader who initiates the trade), which would classify ...

Real-Time Streaming of Every Option Trade

zhlédnutí 17KPřed rokem

After searching for a number of years for a good solution for all my financial data needs, I have finally found ThetaData's API which now provides Real-time Streaming of Options Tick Level Data! In this video we go through how to add all available tick level NBBO trades data to your ThetaData real-time stream. We then explore how you can add only specific contract streams you are interested in,...

Machine Learning in Finance Course

zhlédnutí 16KPřed rokem

Master the most in-demand skill-set of the world's top financial institutions with one of the most practical, comprehensive and affordable courses in Financial Machine Learning. ★ ★ Machine Learning in Finance ★ ★ Release Date: EST 1200 01-Dec Learn more and register your interest here: quantpy.com.au/machine-learning-in-finance-course/ Why I started an online Course? ★ The QuantPy Story ★ If y...

Historical vs Implied Volatility with 10yrs Options Data!

zhlédnutí 15KPřed rokem

In today's tutorial we investigate how you can use ThetaData's API to retreive 10 years of historical options data on Microsoft (MSFT) for comparing Implied Volatility to Historical Volatility. We also describe what the difference between historical volatility and implied volatility actually is. Realized volatility (rv) is the actual stock price variability due to randomness of the underlying B...

Risk Neutral Pricing of Weather Derivatives

zhlédnutí 6KPřed rokem

In this video, we finally use the risk-neutral pricing methodology for valuation of our temperature options in python. In this online tutorial series dedicated to weather derivatives we have estimated the parameters of our modified mean-reverting Ornstein-Uhlenbeck process which defines our Temperature dynamics, and have now implemented different models for our time varying volatility. Now we m...

Can You Compare Intraday Volatility Surfaces?

zhlédnutí 13KPřed rokem

In today's tutorial we investigate how you can use ThetaData's API to retreive historical options data for end-of-day, and intraday trades and quotes. We will create volatility surfaces use an interpolation method (B-Splines) to compare surfaces between the morning (10am) implied volalitity and afternoon (2pm) implied volatility surfaces. Check out ThetaData's API (includes free tier) www.theta...

Monte Carlo Simulation of Temperature for Weather Derivative Pricing

zhlédnutí 8KPřed rokem

In this online tutorial series dedicated to weather derivatives we have estimated the parameters of our modified mean-reverting Ornstein-Uhlenbeck process which defines our Temperature dynamics, and have now implemented different models for our time varying volatility. Now we move on to simulating temperature paths using Monte Carlo simulation method under the physical probability measure. Once...

Time Varying Volatility Models for Stochastic Finance | Weather Derivatives

zhlédnutí 8KPřed rokem

Now that we have a defined the parameters of our modified mean-reverting Ornstein-Uhlenbeck process which defines our Temperature dynamics, in this tutorial we will now be looking to implement different models for our time varying volatility patterns. We have a number of options to model temperature volatility across seasons. - Piece-wise Constant Functions (volatility for each season) - Parame...

Modifying the Ornstein-Uhlenbeck process | A practical application of stochastic calculus for Quants

zhlédnutí 16KPřed rokem

Our goal today is to use our knowledge of stochastic calculus in a practical way to fit a mean-reverting stochastic process to real world data under the physical probability measure. We will attempting to model the variation of the difference between daily average temperature (DAT) and our deterministic seasonal temperature model which takes into consideration temperature trend and seasonality....

Detrending and deseasonalizing data with fourier series

zhlédnutí 19KPřed rokem

Detrending and deseasonalizing data with fourier series

Statistical Analysis of Temperature Data | Time Series Analysis in Python | Weather Derivatives

zhlédnutí 15KPřed rokem

Statistical Analysis of Temperature Data | Time Series Analysis in Python | Weather Derivatives

Introduction to Temperature Derivatives | Weather Derivatives

zhlédnutí 10KPřed rokem

Introduction to Temperature Derivatives | Weather Derivatives

Does Index Fund Investing Still Work in 2023?

zhlédnutí 8KPřed 2 lety

Does Index Fund Investing Still Work in 2023?

The Magic Formula for Trading Options Risk Free

zhlédnutí 20KPřed 2 lety

The Magic Formula for Trading Options Risk Free

You Need to Learn Importance Sampling NOW | Deep Out of the Money Options

zhlédnutí 7KPřed 2 lety

You Need to Learn Importance Sampling NOW | Deep Out of the Money Options

You've been using the Wrong Random Numbers! - Monte Carlo Simulations

zhlédnutí 10KPřed 2 lety

You've been using the Wrong Random Numbers! - Monte Carlo Simulations

Lookback Call Options with Stochastic Volatility

zhlédnutí 3,6KPřed 2 lety

Lookback Call Options with Stochastic Volatility

Pricing Asian Options in the Australian Electricity Market

zhlédnutí 6KPřed 2 lety

Pricing Asian Options in the Australian Electricity Market

Monte Carlo Pricing of a European Barrier Option

zhlédnutí 7KPřed 2 lety

Monte Carlo Pricing of a European Barrier Option

Monte Carlo Simulation with Multiple Factors | European spread options with stochastic volatility

zhlédnutí 6KPřed 2 lety

Monte Carlo Simulation with Multiple Factors | European spread options with stochastic volatility

Stochastic Volatility Models used in Quantitative Finance

zhlédnutí 26KPřed 2 lety

Stochastic Volatility Models used in Quantitative Finance

Heston Model Calibration in the "Real" World with Python - S&P500 Index Options

zhlédnutí 24KPřed 2 lety

Heston Model Calibration in the "Real" World with Python - S&P500 Index Options

Simulating the Heston Model with Python | Stochastic Volatility Modelling

zhlédnutí 24KPřed 2 lety

Simulating the Heston Model with Python | Stochastic Volatility Modelling

Trading stock volatility with the Ornstein-Uhlenbeck process

zhlédnutí 24KPřed 2 lety

Trading stock volatility with the Ornstein-Uhlenbeck process

One question please 17:47, I can do the same algebra on dSt = St(mu*dt + sigma*dWt), then I can also say St also martingale. why is that not correct? Thank you!

This is really, really good. Thanks!

I am a computer science student in Turkey. What should I do please can you share your experiences

The end of content. Curation will be everything

I personally have created a algorithms that works but why would I tell everyone?

At 20:49, if our residuals only show a correlation for the first 15 lags, should we fit a moving average term instead?

Viva la Libertad, Viva la Patria, Viva Argentina 🇦🇷🇦🇷🇦🇷

Hahha someone else will say it's is useless come buy mine... Life is a cycle

Awesome conversation man, thanks for the discussion

Why assuming normal distribution? No black swans, fat tails?

this video is so good!

How does the coding change for American options?

best channel

Great job

how to implement this data for mt4 chart? , how to deploy?

This tutorial is so well done. Thank you thank you thank you!!

i am not sure what i did wrogn but i chose four stocks ['MC.PA', 'AI.PA', 'SAN.PA', 'BNP.PA'] and I got the weirdest looking efficient frontier

hello mate, why is it the timedelta(days=300)? where does the 300 come from ? thanks

thanks you a ton , I have been trying my best to learn but none of the videos strategies worked well from CZcams , but you are a gem .....salute to you as your strategy gave me confidence and growing a lot on demo account and soon I will switch to live account

Great Appreciation and Great Respect to you and your channel!

This is all very fluffy info. Nothing here that will make you money. Also Shelly Natenberg is not a trader. He only discusses theory. If you want to experience real pain go buy some upside calls and sell futures delta neutral against them during a trend day up. You’ll be given no chance to scalp. And by the end of the day you will have lost on your calls and lost big on your futures. While the market maker, who had zero idea where the underlying was going, wins and wins. I’m not saying it isn’t possible to make a lot of money. It is. You have to become an expert is managing risk. This is your edge.

And btw, the best traders on the planet learned their risk management skills by trading the underlying. And not by predicting direction. Nobody can do that with any level of consistency. Options market makers only understand their Greeks and how to manage their risk. A very skilled futures or stock trader will use market makers for what their purpose is. Risk offsets. And, > this is the most important part, parlays. Options give a skilled trader incredible opportunities where you can go from flat to short 200 futures below a line that you can convert and now you’re riding long 200 futures up 10 points with very defined risk. This is very doable way to make $100k a day. And with 0DTE these opportunities exist every day of the week.

but cov matrix is now always invertible (if matrix is not positively defined), so cholesky decomposition does not always work

Hi QuanPy, thanks for the great video! One question do you have any detailed explain or recommended material for the portfolio return at the t, the formula you show up on the right upper corner from 11:35? I know single stock Brownian Motion, but I am not following why portfolio return is in that form and why use timeseries mean return as level. Also should it depend on t as well as BM? Many Thanks!

if you get into Quant trading during a bull market, you will think that you know what you are doing.....till you will find out otherwise......you have greater chances of beating the market if you play old school pacman....(the one with the blue screen) than learning quantitative financial analysis....lol, ..and I kid you not about pacman or space invaders.

Skip the first 7 minutes.

Did he say $300K out of college ? blimey.

Could someone please help me find the website he uses in the video? He says it is free. I am tried a bunch of ways to find it, but I cannot. Does it still exist? Please help

If there is only 1% of a succesful strategy, why there is no 99% of strategies are wining money by only switching the direction of the entry at market?

Hi there, good question. You’re assuming only two outcomes here, up and down and that the direction change is a large enough effect size to make a profit. Otherwise as you are implying you could just short / go the other direction in your strategy and it would be profitable. Once you take into consideration fees (transaction and paying bid-ask spread), you’ll find that very few strategies have a true sharpe ratio that is significantly higher than 0.

Thanks for the GREAT video! One question if I may: at 11:42, would you please elaborate, or if you have another link, for this return formula + Cholesky application? Thanks a lot!

What's the point of complicating matters by throwing in abstractions/ indirections such as covariance matrix and cholesky decomposition, when we can just simulate portfolio returns by calculating cumprod of weighted stock returns directly?

So… around #16:37 … the MLE-estimated mean and variance of a normally distributed set of returns R equal… ("someone has done the hard job for you, they've gone through the math")… the mean and variance of samples r_i…?!? 🤨 Guess I'm missing the point of the entire MLE-concept in this context.

Him: All CZcamsrs offer fake advice on algo trading Also Him: Let me tell you how to trade on this CZcams video The assumption that CZcamsrs have some deep seated ulterior motives, well except for you, is silly.

Well i think non normal error distribution caused by non monotonous growth the chart in a real.. You trying to multiply perfect line and perfect sin() and the modeling chart will growths monotonous while the real one - not. And of course You will get some excesses thant moment the real chart will start to grow like parabolic in average.. As for me thats pretty obviously.. I think the real chart should be additionally averaged, thats makes the average error bigger but makes it close to normal... (There is why You started to talk to try ARIMA like model i think..) Or to try the rose noise, i heard someone using to modeling the stock prices.. But the season decomposition with Fourier i think should be awesome to timing the stock market..

I have a question, If i want to forecast next 4 days in a stock price should i set my T value as T = 4 or T = 4/252

When you divide by 365 @ the end of the 17th minute there, do you not need to divide by 255 (1 year trading days)?

А вообще тяжело здесь подниматься? Только скажите честно, без балды

Tried to run the Jupyter Notebook but EOD returned error message: "Only EOD data allowed for free users. Please, contact our support team"

portfolio_sims meaning portfolio of simulations? Tip: Use the typing module to explain types and use descriptive variables to make sense

Nice! but te music is too loud.

lame

The only ones who are really winning: Market makers and brokerage firms. The others are at the mercy of luck, with inconsistent wins and losses.

error: module is not found for pandas_datareader

does someone have the link to 2rd part of video?

Hi PyQuant! May I know is it possible to simulate stock prices using the same technique? In this video you assume the returns follows multivariate normal distribution and then do the Monte Carlo simulation for returns. I am wondering if I can do the same thing for stock prices by assuming certain distribution such as GBM?

It would be interesting to see how time value is determined.

Newbes may become frustrated by this video ... but ... hes telling truth ... Investors gain success only by developping strategies beyond well known infos and models. Total transparency causes no chance for mechanical/software-driven success. First you have to learn all about common tools and strategies ... then you have to select and check ... then make a decision about your own strategy ... then check the markets for chances ... Dont forget - the closer you stay at mechanical workflows, automated ones the more compettitors you get ... and the more you develop your own system the more risk you take until reality fits to it.

Another clown. Stopped watching after hearing "I will show you my 3 strategies that are guaranteed to make money". What a joke 😂😂

This is more relevant to ML strategies. Good video anyway

Doom is coming for the world get ready worst than corona

As an Algorithmic Trading Quant, which is the most exclusive and cryptic type of Quant, I can objectivelly and without any bias that this role is meant only for men who have an eidetic memory, prophetic vision, omniscient sagacity and a coruscant brilliancy to easily master fields which are by nature both recondite and often out of reach for the common genius. Basically, a quant is a person who has a profitable trading algorithm with a track record which has stood the test of time. Also, if you're a lower class of Quant, you're basically a data scientist or wanker. If you think physics and maths is hard, remind yourself that those guys try to be quants and fail so hard they start to teach physics to PhD.